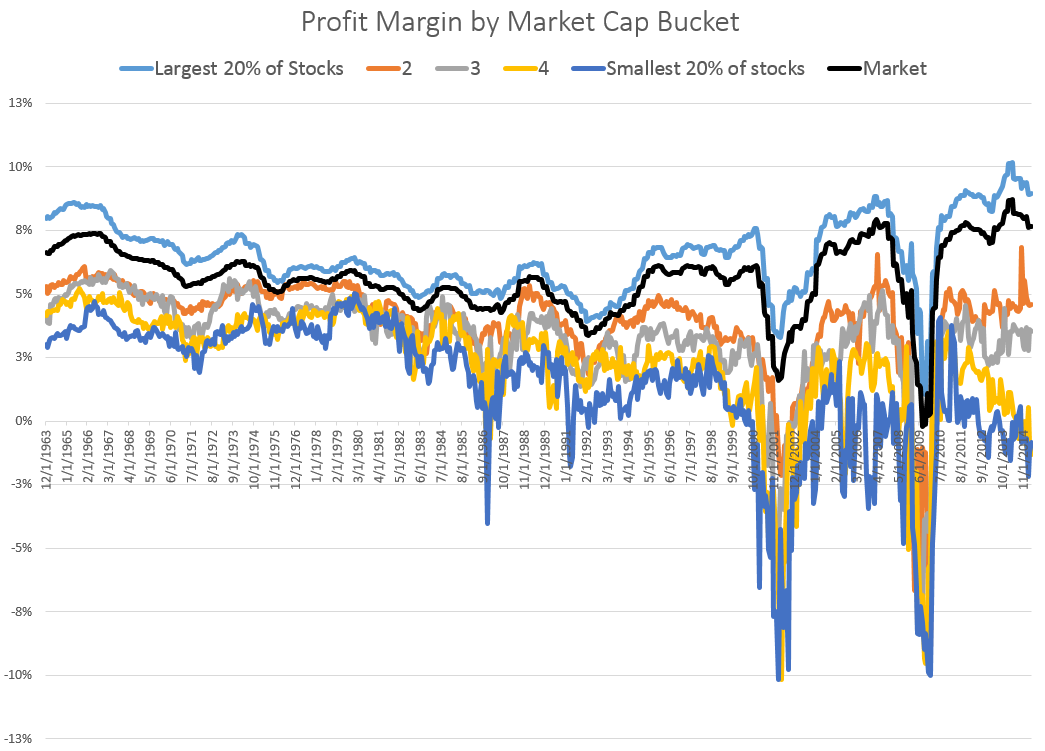

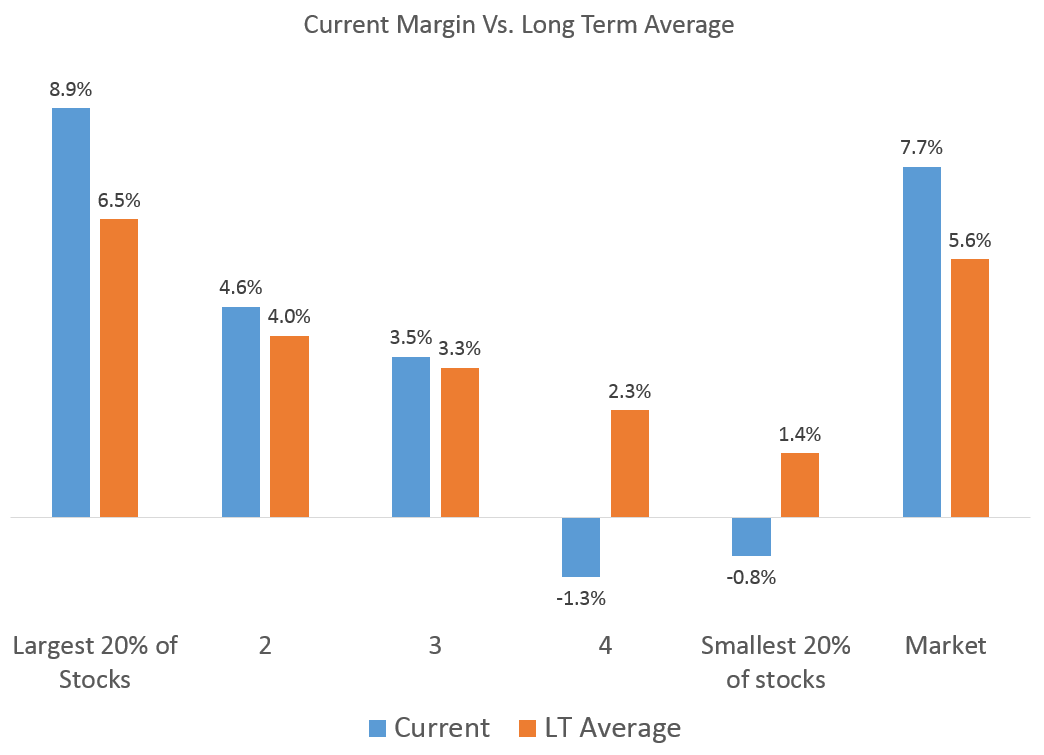

The U.S. market’s profit margin remains very high, but smaller stocks are suffering. While margins for the largest companies have remained well above their long-term averages, margins for the 40% of stocks in the market with smaller market caps have current margins well below their long-term average. This divergence highlights a broader key point: small caps provide unique opportunities and dangers, but are often lost in a market dominated by large caps.

***

The rise of passive, index investing has a funny side effect: a myopic focus on “market-level” statistics. All statistics about the market (profit margin, dividend yield, price-to-earnings, ROE, etc.) are mostly the result of the margins, yields, and valuations of the largest stocks. Apple’s profit margin of more than 20%, for example, has a huge influence on the overall market’s margin. A smaller company that also has a very high current margin-like the biotechnology stock Luminex-has virtually no impact on the “market’s” margin-it is lost in the shuffle.

It is useful, then, to separate the market into market cap buckets (quintiles) to see if the same profit margin trends hold true across the market. Spoiler alert: they do not. (Note: hat tip to everyone’s favorite anonymous genius @jesse_livermore for giving me the idea for this chart, I encourage you to submit ideas like his here!)

While the largest companies have incredible recent profit margins, the average result for small companies has moved the opposite direction: today, these smaller companies have a negative aggregate profit margin.

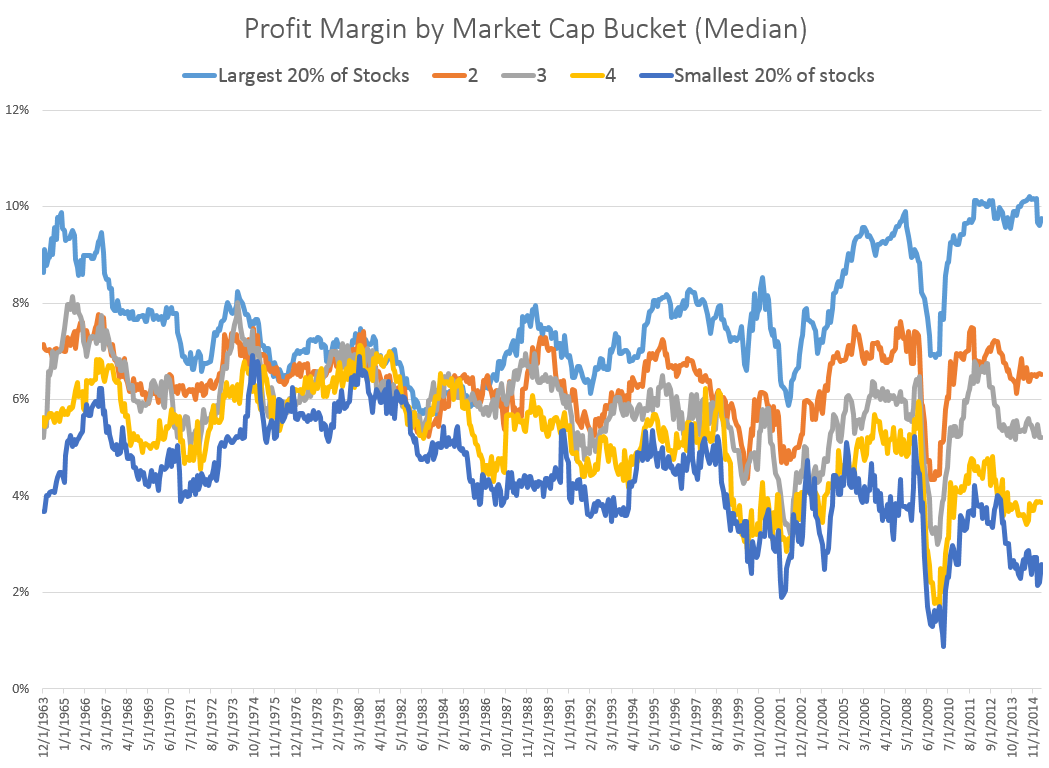

To be fair, these are averages, so outliers can have a large influence on the results. If I removed Cliff’s Natural Resources from the fourth quintile today, the margin for the group would jump from negative to positive.

Still, if we choose median instead of average to eliminate the outlier effect, the same trends persist.

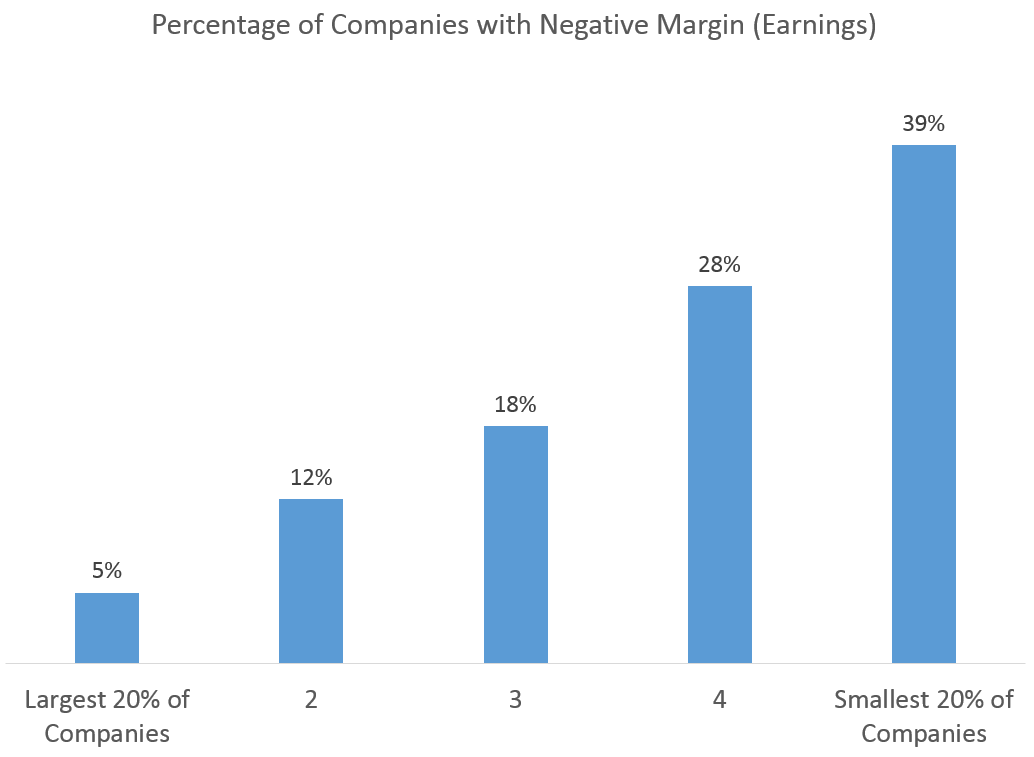

Below averages and medians, we find an even starker comparison. Only 5% of the largest stocks had a negative margin (i.e. negative earnings) at the end of April, 2015, but 39% of the smallest stocks had negative margins.

This evidence once again highlights the unique nature of the small cap segment of the market. In small caps, there is more “junk,” but arguably also more opportunity.

{kind=link}

***

I am a “factor investor” in the sense that I believe in using objective measures to select stocks in a systematic fashion. But I worry that more and more people agree with my preferred method of investing.

It seems that every day I get an email with a new “factor” ETF offering based on the familiar themes of value, momentum, yield, and quality. If everyone agrees that these tilts work (and invests accordingly), then they may stop working.

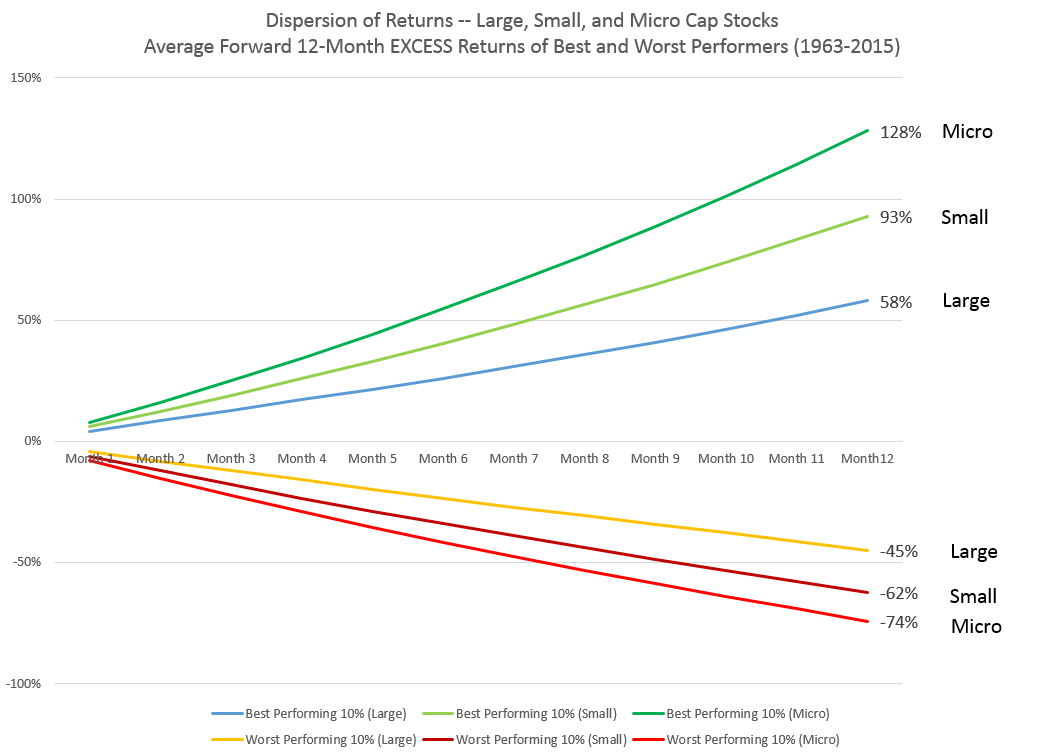

But most active ETFs do not delve into small-cap space because of liquidity concerns. I think this is a good thing for active small cap investors. As more and more investors seek to “arbitrage” the value, quality, yield, and momentum factors, we would be wise to invest part of our portfolio in areas of the market where there are limits to arbitrage. In small caps there are often trends-good and bad-that get lost in market level statistics. In this case, the trend appears negative on the surface (and for these companies, I guess it is). But the silver lining is how different these small companies tend to be. For active managers, different is good.

While everyone focuses on the overall market, we may want to look elsewhere-to beneath-the-radar small cap stocks.

Note: For this piece, I use U.S. domiciled companies only, and require a market cap of at least $200MM, inflation adjusted.

Might this be because smallest caps can go to zero whereas large caps that are in decline will drop out of the large cap bucket to the next one down so you only capture some of the downdraft? And conversely, when the tiny caps do really well, past a certain point they presumably disappear into next bucket up whereas there is no higher bucket for the most successful big caps.

It is difficult to account for drift between buckets. Need to think about an effective way of “tracking” individual names across buckets. As I write more of these kinds of posts, I will keep pondering it. Ideally, the slight “survivorship bias” here would be fully controlled, perhaps by picking annual starting points instead of monthly.

Another thought, maybe the decline over time of profit margin of smallest cap is linked to falling interest rates such that companies can survive longer with lower rates.

Check out my follow up post here http://investorfieldguide.com/the-rich-are-getting-richer/, curious to hear your thoughts (removes the sort by cap)…especially on staples, tech, and financials.

I believe that the evidence is that over many years, small caps outperform large caps and the value trumps growth-again over long periods. Is it possible that Technological improvements have brought us to a new era in which small caps are at a long term disadvantage? Thanks